Get Out of Town With Lazydays Holdings, Inc. (LAZY)

Get Out of Town With Lazydays Holdings, Inc. (LAZY)

How a small RV dealership is making a name for itself...and it's cheap.

Management is experienced and laser focused on deploying their "precious" cash in the most efficient way possible.

An Earnings Power Value calculation shows that Lazydays Holdings Inc is undervalued given current EBITDA and that future growth increases this value.

The main risks to Lazydays Holdings Inc are external and secular and not company specific.

New Dealership Openings Is The Best Return for Shareholders

Lazydays Holdings Inc (LAZY) was founded in 1976 and manages RV dealerships and service centers through various subsidiaries. They exist primarily to sell premium RV brands both new and used while capturing clients for life by also offering parts and services, financing, insurance, campgrounds in addition to new/used RV sales. While there has been much organic growth in their existing dealerships, Lazydays Holdings Inc is opening new dealerships and acquiring existing ones at a rapid pace. While the company is expanding quickly, their balance sheet remains stable. In a Q3 2020 conference call, Bill Murnane is quoted saying, " At present, the returns we can get on new and acquired dealerships are, I would say, multiples higher than any other investment that we have considered." The company put their money where their CEO's mouth was and announced many acquisitions and new openings:

LAZYDAYS HOLDINGS, INC. COMPLETES ACQUISITION OF CAMP-LAND INC.

LAZYDAYS RV OPENS LAZYDAYS RV OF NASHVILLE: ITS 11TH FULL-SERVICE RV DEALERSHIP

LAZYDAYS HOLDINGS, INC. TO ACQUIRE SPRAD’S RV

LAZYDAYS RV ANNOUNCES NEW MINNESOTA DEALERSHIP LOCATION

LAZYDAYS RV ANNOUNCES AIRSTREAM DEALERSHIP IN MINNESOTA

LAZYDAYS HOLDINGS, INC. TO ACQUIRE CHILHOWEE RV CENTER

LAZYDAYS RV ANNOUNCES AIRSTREAM DEALERSHIP IN KNOXVILLE, TN

LAZYDAYS RV ANNOUNCES AIRSTREAM DEALERSHIP IN NASHVILLE, TN

Through Q4 of 2020 and into Q1 of 2021 Lazydays executed on their mission. With all the acquisitions and new investments you would expect corporate debt to be on the rise and rapid asset increase out of line with revenue growth, but this is not the case. Lazydays maintained a strong balance sheet being able to increase their cash position by $32 million over 2019 after spending $79.01 million on investing and financing activities as highlighted in the recent 2020 10K.

The recent slow down in acquisitions, while it is not preferable, I believe is not a major red flag either. Management has expressed in various earnings calls that they are not interested in overpaying simply because their competition is.

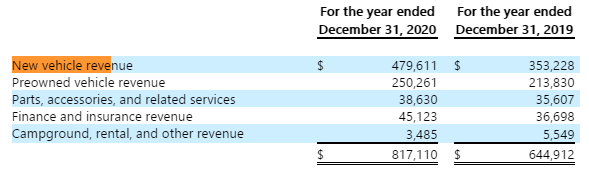

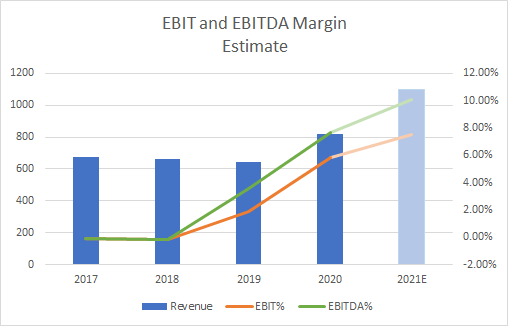

Although the company saw a decrease in Campground, rental, and other revenue, New vehicle revenue, Preowned vehicle revenue, Parts, accessories, and related services and finance and insurance revenue all increased substantially. 2020 saw a 21% YoY increase in revenue snapping the 2017-2019 drop in revenue.

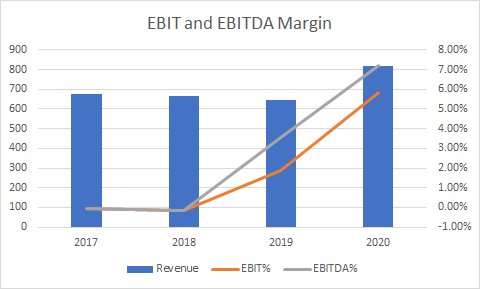

While 2019 was a turning point in operational leverage for Lazydays strong secular tailwinds and Covid-19 accelerated those trends in 2020.

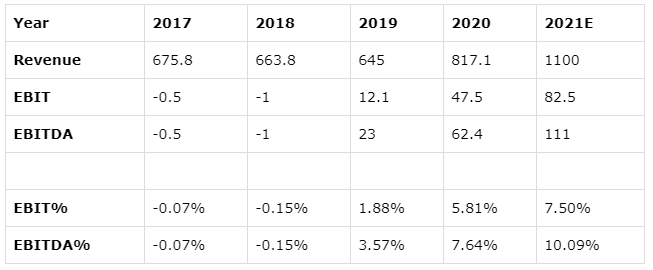

(Source: Author's own calculations from 10-K Fillings)

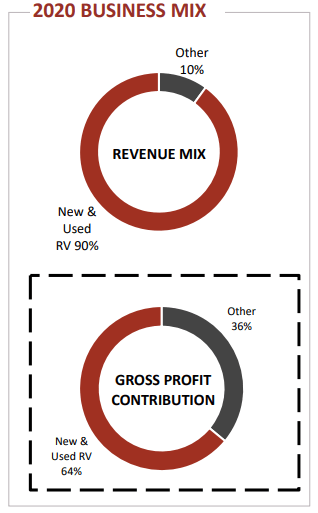

Volume in profitable areas was the key to unlock operational leverage in 2019. Spend some time exploring the investor deck of LAZY and you will find out that though about 10% of their revenue comes from everything other than New and used vehicle revenue, that 10% of revenue is substantially more profitable contributing to the gross margins significantly.

A look back at 2019 though and we see that the profitability of new and used RVs increased about 13% in 2020 relative to the profitability of Lazy's other revenue streams:

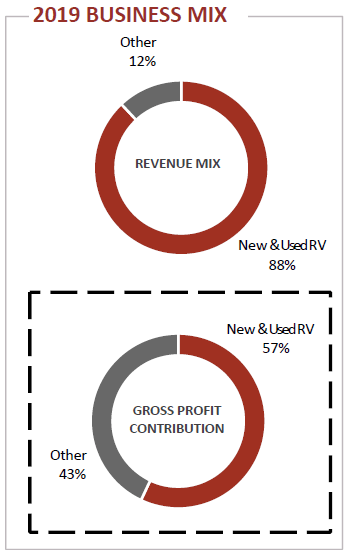

Even though 88% of their revenue comes from RV sales, there is plenty of opportunity to grow the higher profit margin parts of their business.

Valuation

LAZY reported Preliminary revenue of $271 Million, better than analysts expectations, but more inline with investors that understand the demand the RV industry and the auto industry at large is experiencing. First quarter 2021 EBITDA margins were over 10% (10.09% according to my calculations or 10.2% according to LAZY) representing a 25% improvement over 2020 annual EBITDA Margins. This improvement in EBITDA is attributable to increased volume in profitable dealerships, especially the pending sales backlog that is still at historical highs.

As it sits, if EBITDA margins stay the same as Q1 2021 and we assume $1.1 Billion in revenue for the year ($271 Million Q1 revenue times four), LAZY would achieve $111 Million in EBITDA for 2021:

(Source: Data from gurufocus.com and calculations are the authors own. 2021E are authors own estimates)

Simply put with around 20 Million of shares outstanding to represent the total dilution, LAZY is trading at 4.5X 2021E EBITDA at a stock price of $24.58. This represents a value much lower than a closely related industry peer while having slightly superior EBITDA margins compared to CWH. In 2020 CWH had a 9.6% EBITDA margin. Compared to the 10.09% margin LAZY achieved in Q1 of 2021.

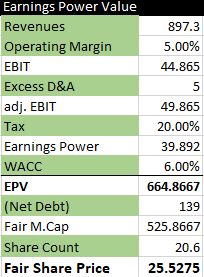

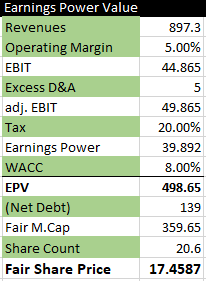

Many articles have already valued LAZY on an EBITDA basis (article 1; article 2; article 3). Below I offer a framework of valuation that emphasizes what LAZY has already done and what it will do. Earnings Power Value focuses on the current earnings ability of a company and does not take into consideration any future growth. Even by these metrics, LAZY is slightly undervalued.

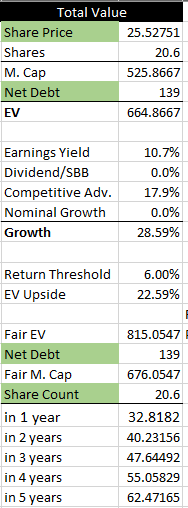

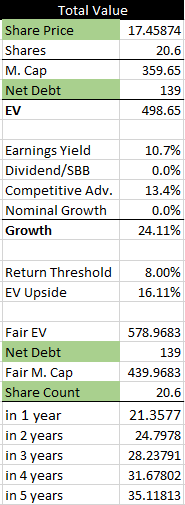

Growth or Total Value, involving the most variables, is the least accurate measure of valuation. Considering an earnings yield of 10.7%, nominal growth of 0% since it is a rapidly growing company, no dividend or share buybacks and 17.6% of growth attributable to LAZY's competitive advantage (more on this below) a price target of $32.81 per share on TTM data is expected.

Estimating eps of $2.62 on a TTM basis LAZY's P/E ratio at current prices would be 9.38 equivalent to a 10.7% earnings yield (1/9.38=10.66%). As far as LAZY's competitive advantage goes, many may not think it is much but the numbers say differently. Given that LAZY has achieved WACCs (cost of equity + cost of debt + cost of preferred) much lower than CWH mainly due to CWH depending on leverage significantly more than LAZY, and earnings that are unrecognized by the industry shown in LAZY's low p/e ratio, LAZY is flying under the radar more efficiently than it's closest competition.

A five year price target of $62.47 represents a 19.6% annualized return. In my opinion, LAZY will appreciate at a rate faster than this given investors appetite to pay for growth and that LAZY's growth adds significant value as long as the company continues to operate at it's current efficiency levels. In the below example, increasing the WACC to 8% representing a 33% increase from my first calculation, really destroys the value that growth adds to the equation:

The main reason this would happen is if LAZY begins to depend on leverage more than utilizing its cash effectively.

My five year price target represents LAZY continuing to fly under the radar relatively unnoticed. If LAZY's earnings and efficiencies are recognized by the market at large, buying LAZY at $24.58 represents an investor paying $0 for the future growth to come.

If you ask me, that is a deal in this market and any market as a matter of fact!

Risks That Could Derail LAZY

Many have mentioned the risk of dilution as a major reason not to invest in LAZY. While no one likes dilution, my analysis takes into consideration the possible dilution that LAZY could have once it's capital structure is cleared up a bit. The risk of dilution should not be a reason one decides not to invest in LAZY at this point.

Another "risk" that some LAZY potential investors point to is merely confirmation bias. Many of those risks are risks to investors because multiple investors point to them as risk. The risk of dilution being one of them and the short interest being another. Taking into consideration dilution into one analysis shows that not to be an issue and, though their is a short interest, that is simply price risk and the fundamentals and earnings of LAZY should put that at rest.

One real risk to consider is the secular trend of the RV industry. To this point, I see LAZY benefitting from a bullish cycle and even a bearish cycle. In a bullish cycle, LAZY can operate with immense agility given its size and capitalization. In a more bearish cycle, LAZY still will be able to grow given it's small size given that acquisitions may be cheaper for the company at this point.

Lazy is well positioned to be a growth company at discounted value prices.

***While this article may sound like financial advice, please observe that the author is not a CFA or in any way licensed to give financial advice. It may be structured as such, but it is not financial advice. Investors are required and expected to do their own due diligence and research prior to any investment.***