Fundamental Research on What Makes Value Investing Tick and The Companies That Match.

Fundamental Research on What Makes Value Investing Tick and The Companies That Match.

Welcome to ResearchForValue. *Good* value investing works.

Sign up now so you don’t miss the first issue.

In the meantime, tell your friends!

So what is all this about? Why in the world do you need another newsletter to read or another email in your inbox?

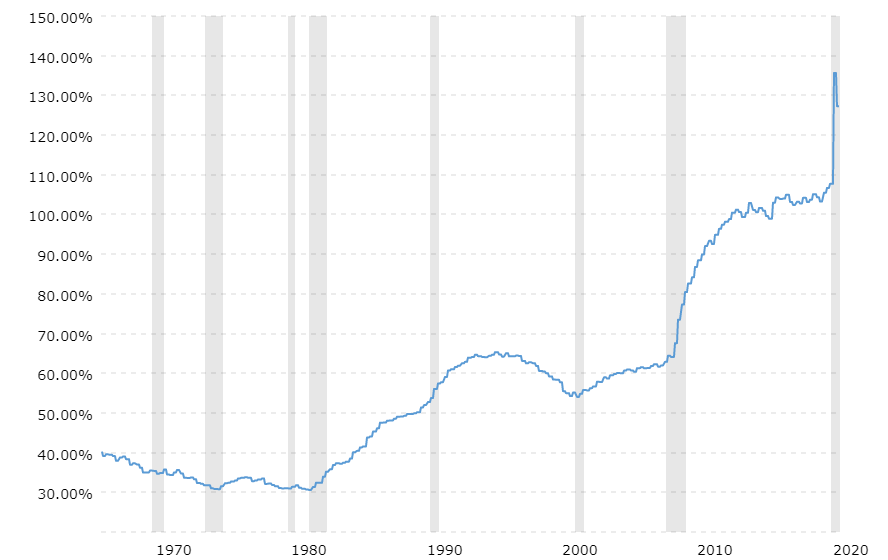

We live in a world moved along by credit and emotion and where popular market indexes shrug of presidential impeachments and major political turmoil.

This could not be more true in the financial markets. What ever we feel like doing can be leveraged with credit.

Debt to GDP Ratio Historical Chart

(Recessions highlighted)

My interest in value investing started merely as a curiosity and has morphed into what I do for a living (amongst other things). One of the fundamental things I have learned about value investing and probably the main reason I am attracted to it is just how antithetical and contrarian it is (maybe it’s a personality fault!). Contrarian thinking alone though does not produce a viable investment thesis:

A contrarian approach is just as foolish as a follow-the-crowd strategy. What's required is thinking rather than polling. - Author: Warren Buffett (emphasis is mine)One example of contrarian thinking with value investing is as the price of a company, or bond, or automobile, or art that is worth investing in goes down your risk goes down as your potential return goes up. This is opposite of the common thinking that high risk equals high return. I believe this type of investing is not only ageless but the best type of investing you can do. This is not true for poorly managed, researched and understood companies.

In various ways I plan to highlight this anomaly (and others like it); to provide a different lens in which to view finance, investing and money habits.

What are your credentials? Why should I listen to you?

Much of what I have learned has been by independent reading and research. I make no efforts to separate my self as a self-proclaimed expert. I don’t have a formal education in finance. I went to a small Christian private university in Arizona and majored in Biblical Studies emphasizing in the Biblical Language and Exegesis (essentially a linguistics degree and a fancy word for interpreting literature). It is a mouthful, but it taught me much that can be applied to finance. How to be a critical thinker, understand history, how to argue persuasively, to write, how to do research and how to acknowledge the faults in your knowledge. These are fundamental skills that I think aren’t taught in many business degrees or economic programs that are essential to the value investor’s thinking.

In addition, I have worked essentially as an analyst at a small RIA for three years.

Isn’t value investing out of favor?

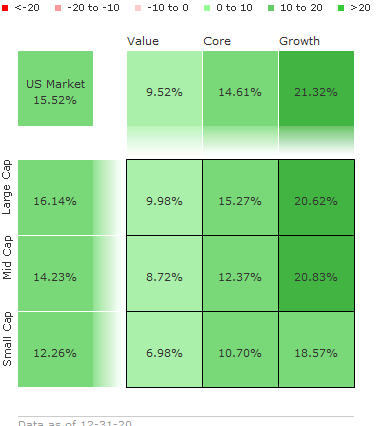

Facebook, Amazon, Netflix, Google, Tesla…Names that you have heard over and over again and dominate the investment landscape at a popular level and even some institutions. I am not going to comment here on these companies on whether they are a good value or not, but I will mention that companies traditionally understood as value stocks haven’t performed as well in recent times. Morningstar has a helpful style box that shows how traditionally understood value has underperformed growth over a 5 year period (returns are annualized).

On the other hand there are many value investors today, many that you haven’t heard of that perform extremely well over the same time frame and almost anyone would be happy to have them manage his or her money.

Like any profession, constant learning and evolution is required to stay on the cutting edge to keep ideas fresh and relevant. While the Graham-Buffet era of investing, where we look for amazing brands with p/b ratios below 1 *may be* behind us (though I am not certain about that!) the runway for value investing is still long and has many iterations and generations of investors to capture with its simplicity, discipline and excellent results.

You may notice at the top of the page I noted that *Good* value investing works! That statement couldn’t be more true. For every good value investor, there is 10 or so bad ones. I plan to focus on the good, learning from the bad, studying the generations before me and share it with you all.

How often will you bug me?

Hopefully never. I hope to deliver thoughtful, fun to read, well synthesized research on companies (or other investments) or investment related topics, about once a week, say every Monday? I will give you a heads up on any changes.